Which is better as a hedging instrument?

An option or a forward?

While both can protect your business from the vagaries of the markets, it doesn’t follow that either will do, regardless of the situation. In fact, under certain conditions, your choice of hedging instrument could be make or break.

The airline industry learned this the hard way in 2020.

For decades, airlines have used either options or forwards to hedge fuel costs. Or, if they used a mix, it wouldn’t be an even split. One instrument would make up the bigger proportion of the hedge.

That worked (mostly) well until Covid-19 — a one-in-a-century bolt out of the blue — hit. And the airlines that had backed the wrong horse hedging strategy lost billions of dollars.

Here’s what went down.

That price ain’t right: why airlines hedge fuel

Airlines hedge fuel for one simple reason: it’s critical to their survival.

With soaring ticket prices, eye-watering surcharges, and in-flight meals that make prison food seem like Michelin-starred fare, you’d think airlines would be raking it in. But the truth is that profit margins are razor thin, mainly due to fuel prices.

Statistics from IATA, the International Air Travel Association, show a direct correlation between fuel and profitability.

In 2018, fuel made up around 23.5% of airlines’ total expenses and the average profit margin was 5.8%. Fast forward to 2019, and a 1.5% increase in the cost of fuel slashed profit margins by 0.8% — a reduction in profits of $3.4 billion over the previous year.

Fuel has such a big impact on airlines’ profitability for two reasons.

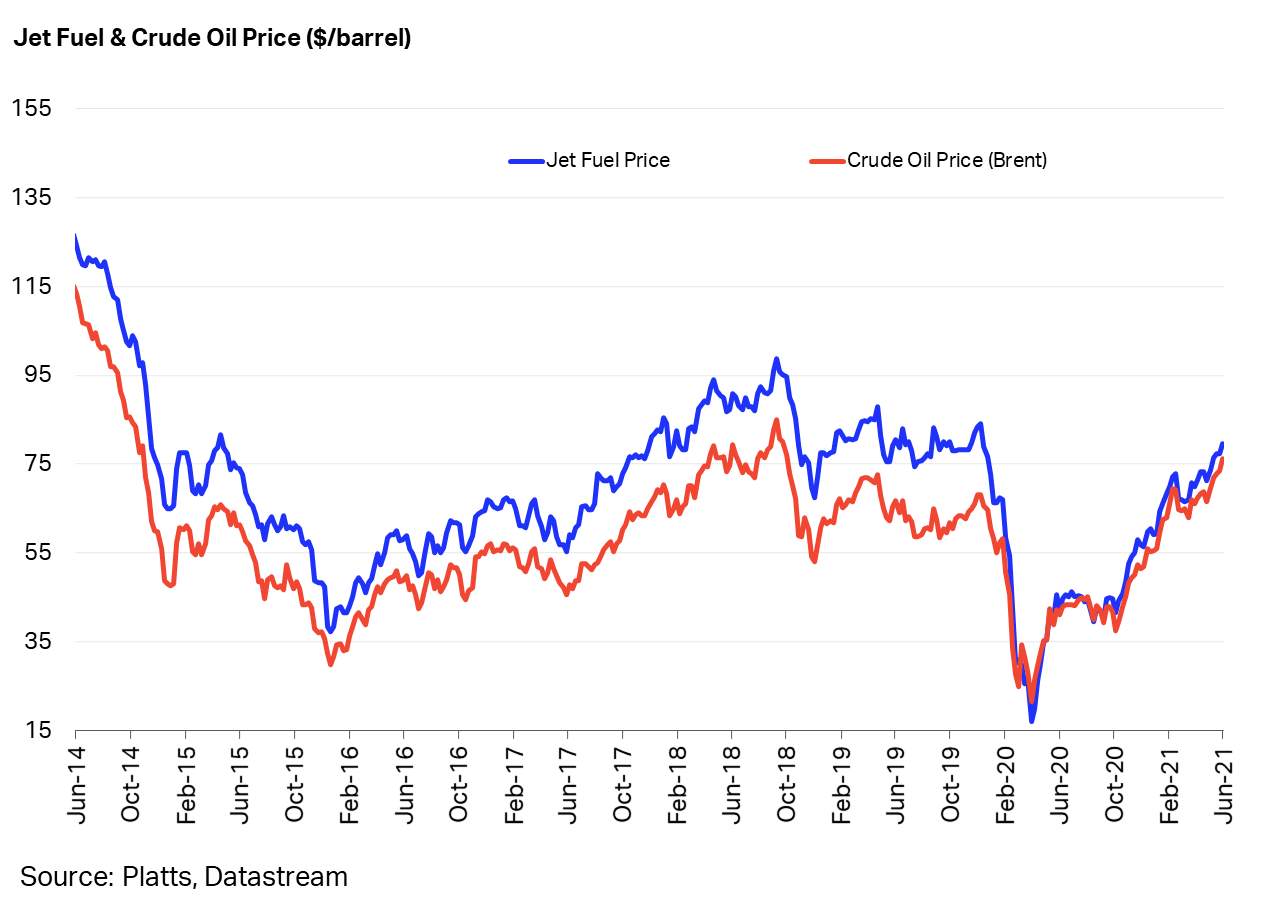

Firstly, the price of oil is infamously volatile.

Soaring or tumbling prices have plunged the global economy into crisis on multiple occasions. So it’s not hard to see how even relatively small movements could raise fuel prices to an extent that risks completely wiping out airlines’ profits.

Secondly, fuel is always priced in US Dollars.

If you trade mainly in a different currency, and the exchange rate with the Dollar becomes unfavourable at the same time as fuel costs rise, it’s a double whammy. Fuel costs more. Dollars cost more. And your profit margin takes an even bigger hit.

That’s where options and forwards come in.

Instead of purchasing fuel at whatever the going rate is, airlines can lock in the price of their future supplies.

This creates certainty. With a good price secured, an airline can budget more accurately for the financial year ahead and shield themselves from market movements that could be hugely damaging to their financial health.

But hedging also benefits the customer. If the price of fuel is predictable, airlines can keep their ticket prices at a reasonable level, instead of being forced to hike them up every time the price of fuel rises unexpectedly.

Forwards vs options: what’s the difference?

Both forwards and options give you the right to buy x amount of a commodity — in this case, fuel — for x price on x date. But this is where the similarities end.

A forward is a legally binding contract. So, when you enter into this kind of arrangement, you have to buy the amount of fuel you’ve agreed to buy, for the price you’ve agreed to buy it, on the date in the contract.

Whether you want to or not.

By contrast, an option gives you a choice. You can go ahead and buy the fuel for the agreed price. Or you can choose not to proceed on these terms.

Clearly, an option is the more flexible choice.

Imagine you agreed to buy 100,000 litres of fuel at $1 a litre on the 10th June 2021.

On the 25th June, the price of fuel goes down to 50c a litre. You also realise you actually need 50,000 litres of fuel, not 100,000.

If your agreement is a forward, tough luck. You’ve no choice but to fork out the full $100,000 — double what you need for double what you’d pay on the open market.

But if your agreement is an option, you can just ignore it, buy 50,000 litres for 50c a litre on the open market, and save your business $75,000. Happy days.

‘So why don’t all airlines go for options over forwards when they hedge?‘ you might be asking.

Well, it’s a question of risk and reward.

While options are flexible, that flexibility comes at a price. To enter into an option agreement, you have to pay a non-refundable premium. This covers the other party’s costs should you decide not to exercise your option.

With forwards, there is no non-refundable premium since the agreement is binding and the other party has a right to enforce it if you try to pull out. Nonetheless, using forwards does require capital, too. There is a security deposit (initial/variation margin) to pay, and in the event of adverse margin movements there is always the risk of a ”margin call” – a demand to deposit further capital to cover possible losses.

So business judgement is critical to weigh up these risks and rewards.

On the one hand, you might reason that you never know what might happen. So it’s worth paying a small premium in exchange for being able to keep your options open.

On the other, you might decide that, based on last year’s ticket sales and flight schedule, it’s safe to assume you’re definitely going to need X litres of fuel at some point.

So why needlessly incur the additional cost of an option premium?

The ‘Rona bites

The latter line of reasoning went out the airline industry’s collective windows on 11 March 2020, when the World Health Organisation declared Covid-19 had become a global pandemic.

With the vast majority of countries worldwide enforcing lockdowns to stop the spread of the virus, 2020 would go on to become the worst year for passenger numbers in the history of air travel.

But lockdowns and other restrictions on social contact also had another effect.

With travel, factories, and most other sectors at a standstill, demand for oil tanked too. This created such a huge oil surplus that the world almost ran out of storage space. And the price of oil hit negative territory for the first time in history.

For airlines who had hedged using primarily options, they had to forgo the premium they paid, resulting in losses. But, on the flip side, they were not obliged to buy fuel at historical, higher prices, nor were obliged to buy more fuel while their fleet was grounded. Moreover, really savvy airlines who had avoided forwards could load up on 5 year options while the price had crashed to $20 a barrel from a peak of over $85.

But for airlines that relied on forward contracts, the news was cataclysmic.

The legally binding nature of these agreements meant they still had to take delivery of the fuel and pay the agreed price. And eye-watering losses ensued.

The table below compares the losses of three airlines that hedged using mainly options to three that hedged using mainly forwards:

The times… are they a-changing?

It’s safe to say Covid-19 has given the airline industry a crash course in the dangers of being complacent.

Options may have seemed needlessly expensive when passengers were flocking to airports.

But now that airlines have racked up billions of dollars in losses because they hedged using forwards, options must seem very cheap. Which goes to show it’s all a matter of perception.

Will these airlines all change tack and start using options over forwards from now on?

We can only speculate.

The good news is that you can learn from their mistakes.

There’s an old adage that says you should hope for the best, but prepare for the worst.

So, if you want to make sure you’re truly prepared for the unexpected, isn’t it worth paying the small upfront premium for an option, if it can help you avoid a much bigger loss?

Markets are predictably unpredictable.

Find out how one of our partners can help – powered by our technology platform.